How To Find New Crypto Coins? Finding Cryptocurrency Projects

%201.svg)

%201.svg)

Click here to buy Cryptocurrencies from Gate.io

If you are wondering how to find new crypto coins, this is the place to be.

Finding new crypto coins has become important since the rise of Bitcoin and the wealth gained by early investors. The crypto market has experienced a surge of new investors who hope to find the next big coin, but many are unsure of how to navigate the space and identify new coins. It can be exciting to discover new coins, but it's important to beware of scams like the Squid token that exploited the popularity of the Squid Game movie series. Before looking for new crypto coins, here are some points to consider before making an investment decision.

Checklist Before Investing:

A project's whitepaper is a good starting point for researching a new crypto project. Most new crypto projects have a whitepaper or official document that includes information such as the project's use case, tokenomics, team members, and roadmap. The presence or absence of a whitepaper can tell you a lot about the project's seriousness. While reading a project's whitepaper, there are a few things to look out for:

Use case: This is the main problem that the crypto project is trying to solve, or its unique function. For example, there are several Layer 2 projects that aim to improve the low latency and transaction times of traditional blockchains without compromising security and decentralization.

Tokenomics / Token Economics: This is the basic plan for how the project's new crypto tokens will be distributed. This includes how many tokens will go to the founding team, advisors, how many will be available for sale to the community, how many will be in the treasury, and what type of token it will be (deflationary or inflationary, with a limited or unlimited supply).

Lock-up period: This is the period of time that the founding team agrees to lock up their tokens before they can access them. A longer lock-up period can give investors more confidence in the project's long-term commitment.

Founding team: It's important to check the background of the project's founding team. Are they experienced, do their backgrounds match the project, and do they have any fraudulent history with past projects? The profiles of the advisors and investors/backers of the project can also be useful.

Social virality: Decentralization is at the core of crypto, so projects are often community-driven. The growth of the project's community can be a good indicator of investor confidence. Twitter, Telegram, and Discord are popular platforms for building crypto communities.

Roadmap: The project's roadmap contains its major plans and timeline. This can indicate the project's seriousness, especially when compared to what they have accomplished. Have they achieved any of the earlier plans on the roadmap within the specified timeline?

In addition, looking at the number of people on the project's watchlist, and whether it is listed on CoinMarketCap.com or CoinGecko, can also be a good confidence booster.

Click here to buy Cryptocurrencies from Gate.io

How to Find New Crypto Coins

Before new crypto coins are listed on exchanges, they are often first offered as Initial Coin Offerings (ICOs), Initial Exchange Offerings (IEOs), or Initial Dex Offerings (IDOs). These offerings give investors the opportunity to get in early on projects before they go mainstream. This is where early investors can get into major projects before they are listed on crypto exchanges.

There are several platforms that feature upcoming crypto projects, including:

- Top ICO List: This website provides white papers and one-pagers of ICOs of new crypto coins. You can find a comprehensive list of ICOs and information on some of the best ICOs in the market, as well as information on past ICOs to use as a benchmark for evaluating the performance of ICOs you are considering.

- CoinGecko: This is a useful tool for crypto traders and investors to stay up to date with the market. It provides real-time prices of cryptocurrencies from multiple exchanges, as well as other important information about different cryptocurrencies, such as their historic performance data, community, and insights into the coin development. CoinGecko also provides an ICO list of new crypto coins with relevant information about the new crypto coin/project.

- CoinMarketCap: Like CoinGecko, CoinMarketCap is an alternative that some investors use to find new crypto coins. It provides a list of ICOs and relevant information, as well as information on hundreds of other crypto projects and actionable data. The watchlist feature is also useful for seeing how many people are interested in a project.

- ICO Bench: This is a useful tool for finding new crypto coins. ICO Bench is an ICO grading website that uses crowdsourced ratings from crypto traders and experts. The experts evaluate projects using various parameters and grade them accordingly.

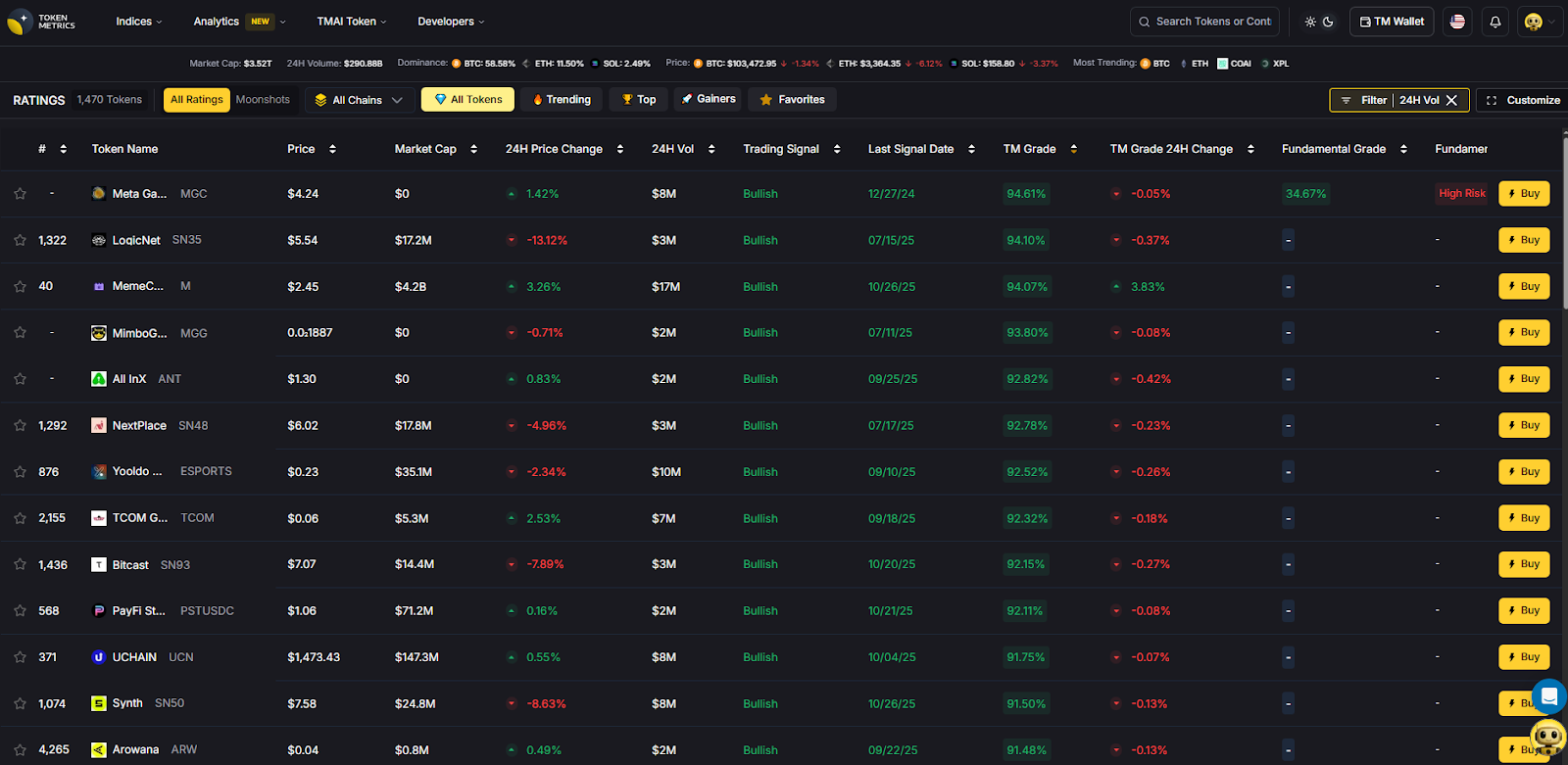

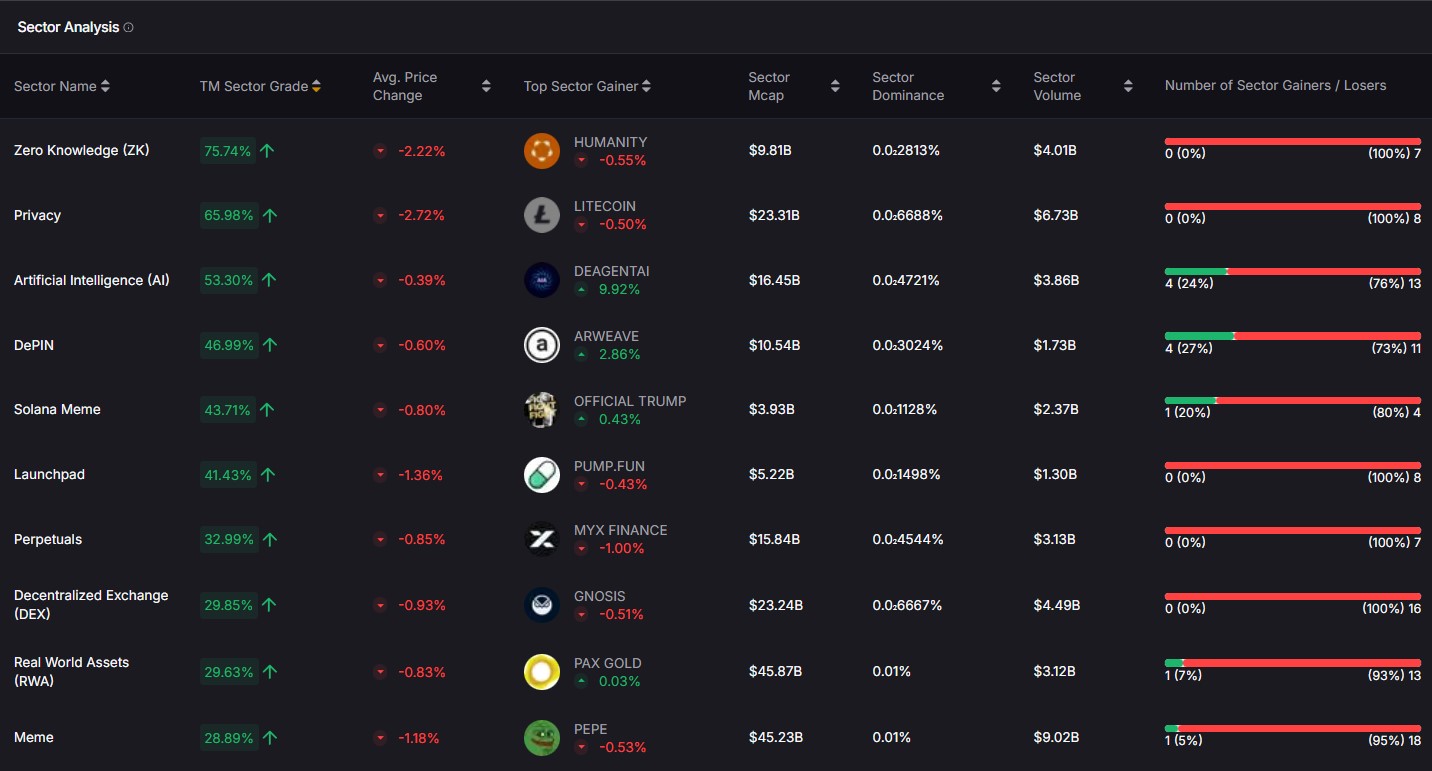

- Token Metrics: Token Metrics is another great resource for finding new cryptocurrencies with its research, deep dives, AI, and more. The best part is that you can use Token Metrics to evaluate whether the newly found project is good or bad and decide whether you should spend more time researching it further.

With over 10,000+ crypto coins, there are many opportunities out there. But there are also many shady platforms and crypto projects, so it's important to know how to find crypto with potential and make sure the projects are viable. Using the tips above can help you do that.

Click here to buy Cryptocurrencies from Gate.io

AI Agents in Minutes, Not Months

.svg)

%201.svg)

.png)

.svg)

No Credit Card Required

Online Payment

SSL Encrypted

.png)

Token Metrics Media LLC is a regular publication of information, analysis, and commentary focused especially on blockchain technology and business, cryptocurrency, blockchain-based tokens, market trends, and trading strategies.

Token Metrics Media LLC does not provide individually tailored investment advice and does not take a subscriber’s or anyone’s personal circumstances into consideration when discussing investments; nor is Token Metrics Advisers LLC registered as an investment adviser or broker-dealer in any jurisdiction.

Information contained herein is not an offer or solicitation to buy, hold, or sell any security. The Token Metrics team has advised and invested in many blockchain companies. A complete list of their advisory roles and current holdings can be viewed here: https://tokenmetrics.com/disclosures.html/

Token Metrics Media LLC relies on information from various sources believed to be reliable, including clients and third parties, but cannot guarantee the accuracy and completeness of that information. Additionally, Token Metrics Media LLC does not provide tax advice, and investors are encouraged to consult with their personal tax advisors.

All investing involves risk, including the possible loss of money you invest, and past performance does not guarantee future performance. Ratings and price predictions are provided for informational and illustrative purposes, and may not reflect actual future performance.